|

|

| |

April 2017 SEE Monthly Update

Permania

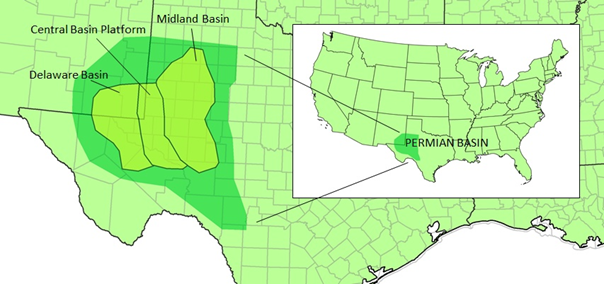

The title of this month’s SEE analysis, used by a recent conference speaker, accurately captures the white-hot level of continued oil producer interest in the Permian Basin, pictured above.

The US strike on Syria after Syria’s chemical gas attack on its citizens does not change the supply-balance equation except as a reminder of roiling Middle Eastern politics. Nonetheless, the follow-on will be important particularly if Iran or Russia gets more aggressively involved. And, the action reminds us about the United States’ improved global strategic position now that we import fewer barrels of oil while producing and exporting more oil and products. Also recall that after our own production our largest oil supplier is Canada, not Saudi Arabia.

Is the Permian the world’s biggest oilfield? Bigger than Saudi Arabia’s Ghawar? Bill Marko of Jeffries claims it is. What’s clear is drilling’s recovery from last year’s lows, with March’s crude oil and lease condensate of 9. 1 million barrels per day (MMBPD) just under the year-ago level of 9.2 million barrels per day. The Baker Hughes oil rig count has increased from 372 on March 25, 2016 to 652 on March 24, 2017. And while oil in storage in March was at historically high levels of 533 million barrels, natural gas in storage has eased off of year-ago levels by 16%, or 400 billion cubic feet, providing more price support than last year as we go into the spring shoulder season.

One drilling cost and operation receiving special attention is water: water transportation and handling, water for fracturing, and wastewater treating for both flowback and produced water. The lowest Permian ratio of water to oil mentioned was 1:1, typically, far more water than oil comes out of any given well. This is not just flowback water (return of the water that went into the well for fracturing), but also produced water, which is salty and contains lots of solids, requiring substantial treating. For more detail on new estimates of Permian acreage value, log in or subscribe.

More information can be found in the subscriber section. For more information, log in now or, if you are not already a subscriber, subscribe now.

Copyright 2017, Starks Energy Economics, LLC. This information may not be disclosed, copied or disseminated, in whole or in part, without the prior written permission of Starks Energy Economics, LLC. This communication is based on information which Starks Energy Economics, LLC believes is reliable. However, Starks Energy Economics, LLC does not represent or warrant its accuracy. This communication should not be considered as an offer or solicitation to buy or sell any securities.

- Complex PADD III Gulf Coast Refineries Benefit, March 2017 (03/2017)

- Sand (and Proppant) Storm, February 2017 (02/2017)

- SEE PADD II & IV Refineries, January 2017 (01/2017)

- Permian Part II: Hottest Basin, and New Administration, December 2016

- Permian Basin Part I, Inventories, Election, November 2016

- Favorable Winds? Harvesting This Alt Energy Source No Longer Quixotic, October 2016

- Exploration Activity Focuses on Permian Basin, Earthquakes, September 2016

- Petroleum Market Suffers from Inventory Surplus, August 2016

- Many Still Producing Natural Gas in PA-OH Marcellus, Late June/July 2016

- Sand & Proppant Companies Squeeze Through Decline Funnel, June 2016

- Gulf Coast (PADD III) Refining, May 2016

- California Refining, April 2016

- Low Natural Gas Prices Benefit Utilities, March 2016

- Do Solar Energy Companies Shine?, February 2016

- Oil Export/Energy Bill Winners and Losers, January 2016

- Permian Persistence, Part II, December 2015

- Permian Persistence, Part I, November 2015

- Life at the Pumps: Gasoline Demand-Analysis in Two Graphs, October 2015

- Whale Watch: Dividend Hunting at Integrated Internationals, Late September/Early October 2015

- Enduring the Downturn; Bakken Resilience - August 2015

- California Refiners - July 2015

- Bakken Producers, US vs. OPEC vs. Russia, Epstein book - June 2015

- Investor Momentum, Oklahoma Earthquakes, Bakken Rail Transport - May 2015

- Regulatory Changes, Earthquakes, and Proppant Companies - April 2015

- Who is Hurt and Who Benefits from the Oil Price Drop? - March 2015

- Oil Field Services Stress Tested - February 2015

- Haynesville, Louisiana Dry Natural Gas Field - January 2015

- Is the Permian a Bargain Basin Yet? - December 2014

- Starks Energy Economics on Natural Gas - 4th quarter 2014

- Eagle Ford Energy - 3rd quarter 2014

- The Power of the Permian - 2nd quarter 2014

- Ethylene, Star Petrochemical with Renewed Luster - 1st quarter 2014

- Pipeline Drag Reducers - 4th quarter 2013/1st quarter 2014

- Signal vs. Noise: Energy Sources Fueling the United States Now - 3rd quarter 2013

- Natural Gas: Heating, Electricity, Industrial Use, Transport Fuel, Export, or All of the Above? - 2nd quarter 2013

- Besides Better Weather, What Does It Take to Operate an Oil Refinery on the US East Coast? - 1st quarter 2013

- Oil Industry in North Dakota Continues Booming - 4th quarter 2012

- Low First-Half Natural Gas Prices Help Clean the Air - 3rd quarter 2012

- Permian Basin, West Texas and New Mexico - 2nd quarter 2012

- US MidContinent Refineries - 1st quarter 2012

- North Dakota's Bakken Oil Shale Production - 4th quarter 2011

sitemap | home | contact us | bio | links | events

|

|

|